RECAP: 2018 FOX Family Office Forum

| Presenters: Jesica Speer, Senior Manager, Private Wealth Services, Grant Thornton LLP Session Description: Since the Tax Cuts and Jobs Act was released at the end of 2017, family office professionals have been struggling to understand the implications for their clients. These industry experts discussed the opportunities the tax law has created and the practical strategies they recommend for making the most of the current tax climate. Topics addressed in this session included: gift planning and higher estate exemption exclusions, entity restructuring options, deductibility of trust expenses, investment expenses, investment interest, and donations to charity. |

- The Tax Cut and Jobs Act of 2017 ushered in the most significant overhaul of U.S. tax code since 1986, and will have a profound impact on individuals, trusts, estates, and businesses. The tax law alters individual income taxation, reduces corporate income tax, introduces a new form of taxing pass-through income, and doubles estate tax exemption and GST exemption to $11,180,000.

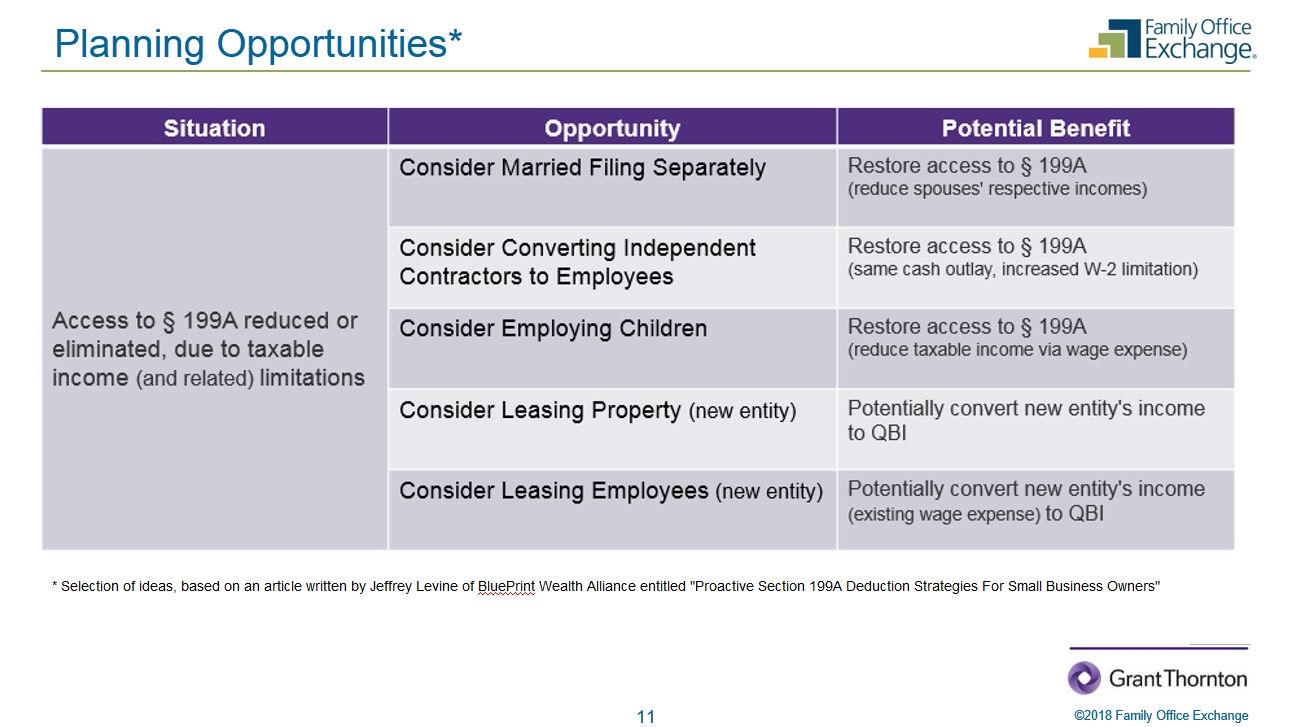

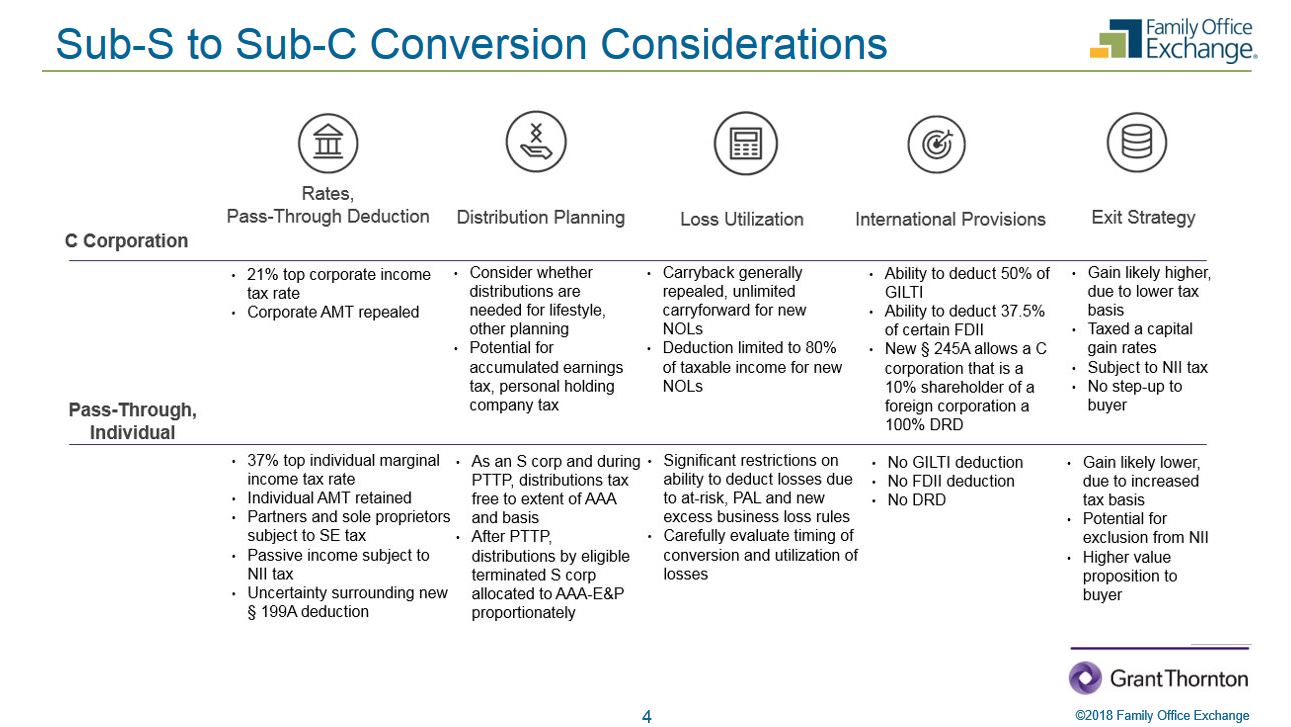

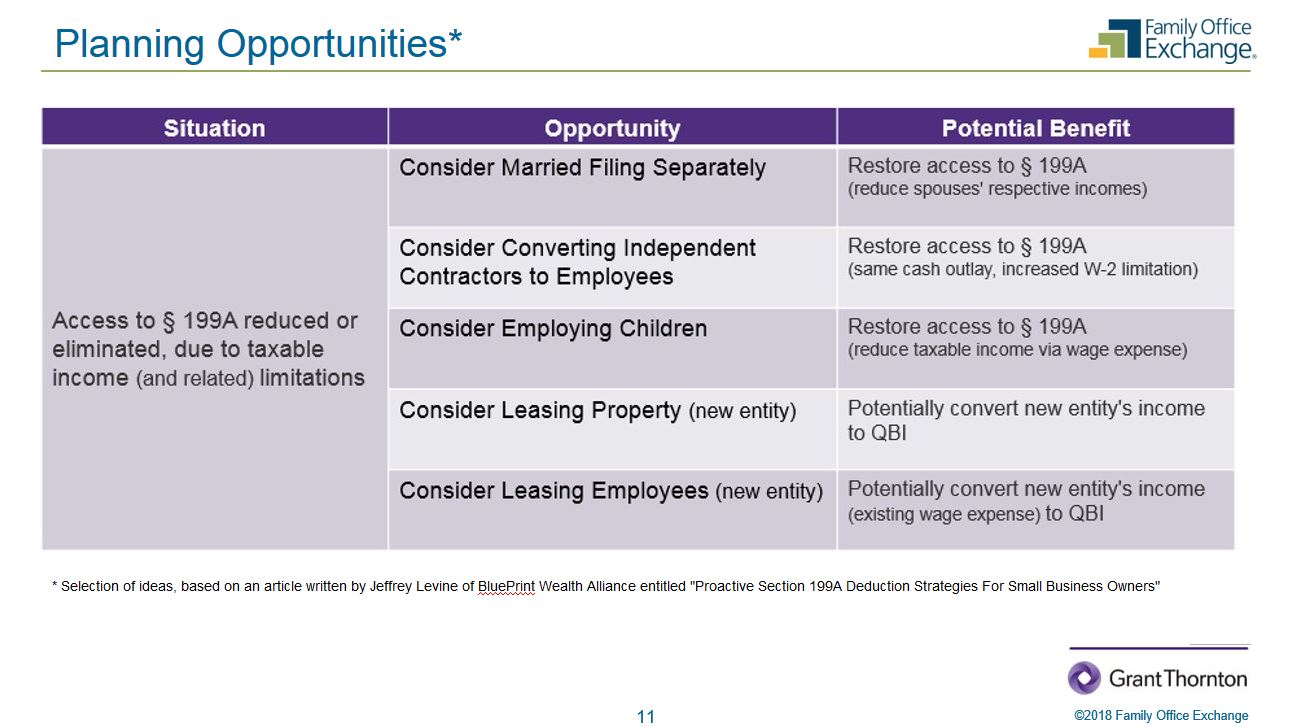

- On business tax issues, the tax law changes prompt consideration of moving from an S-Corporation to a C-Corporation to take advantage of provisions within the law on pass-through deduction, distribution planning, timing, and utilization of losses and provisions around international holdings. Changes to rules on pass-through deduction warrant consideration on rental properties, multiple businesses, tiered entities, allocating W-2 wages, and interaction with other loss limitation rules. Tom Abendroth of Schiff Hardin cautioned everyone to consider the all-in costs of structure changes.

- The decision to move from an S-Corporation or partnership to a C-Corporation is complicated. There is no one-size-fits-all approach, and Jesica Speer of Grant Thornton encouraged participants to work closely with their legal and accounting professionals to make this decision.

- The decision to move from an S-Corporation or partnership to a C-Corporation is complicated. There is no one-size-fits-all approach, and Jesica Speer of Grant Thornton encouraged participants to work closely with their legal and accounting professionals to make this decision.

- Limits to the state tax deduction are significant depending on the state of residence. Many families, especially in high tax states like California and Illinois, are thinking about changing domiciles.

- Section 67 (e) continues to allow miscellaneous itemized deductions for expenses associated with property being held in trust, including: trustee fees, legal fees related to administration of trust or estate, tax return preparation, appraisal, fiduciary accounting costs, state taxes (up to $10,000), and interest and other expenses based on the same rules as applied to individuals. Also, tax law changes included a repeal of the “Pease limitation,” which increases the benefits of charitable giving.

- Estate planning exclusions were raised to $11,180,000, which is a significant increase over prior years. Recommendations include a review of allocations in wills and trusts based on “maximum applicable exclusion” or the “maximum GST exemption” to avoid unintended consequences. For ultra-wealthy estates, use and leverage the exclusion to “supercharge” the benefit of lifetime transfers. However, a technical corrections bill and IRS guidance are still to come, so there is no need to rush.

Download the Session Presentation >

(FOX Members only)

Session Recaps

| Technology Solutions |